Canada's $5.5B Cannabis Market: Delivery Drives Growth

10 hours ago 26

Eight years after Canada became the first G7 nation to legalize recreational cannabis nationwide, now the industry is entering a new phase. Product selection remains important, but as competition increases and retail markets mature, convenience is becoming one of the industry's strongest differentiators.

Consumers increasingly expect the same seamless purchasing experience they receive in other retail sectors: online ordering, fast fulfillment, and reliable delivery. As a result, many cannabis businesses are investing less in expanding physical footprints and more in the infrastructure that helps products reach customers quickly and efficiently.

That shift is helping redefine how retailers compete—and why delivery is emerging as one of the most important growth drivers in Canada's legal cannabis market.

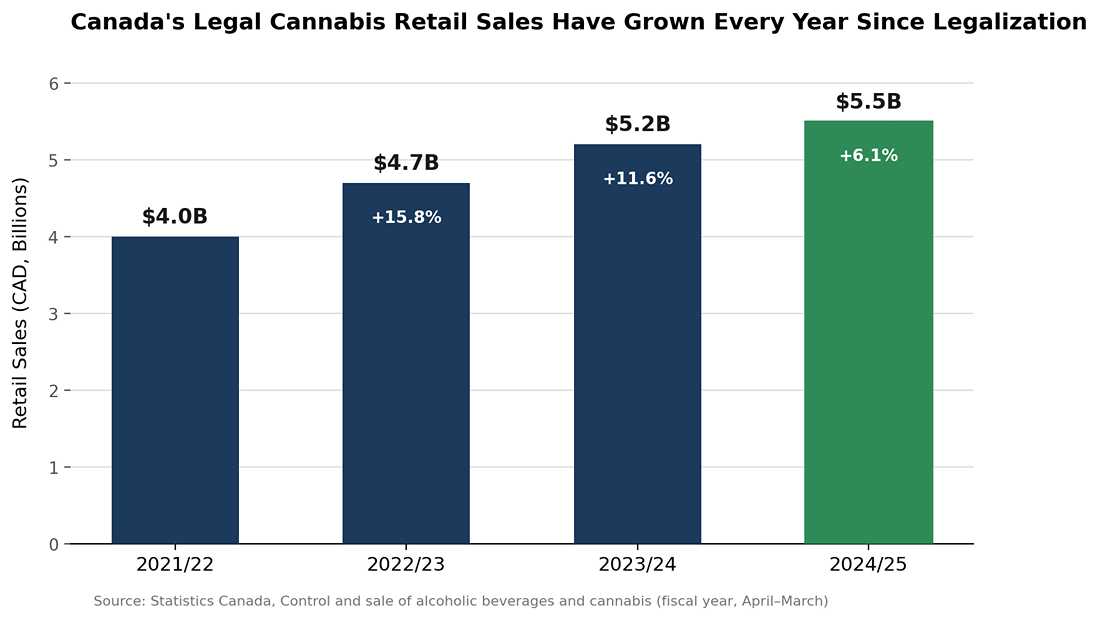

Statistics Canada reports that legal cannabis sales rose 6.1% year over year to $5.5 billion in the 2024/2025 fiscal year, up more than a third (37.1%) from three years earlier. Federal and provincial governments collected $2.5 billion in tax revenue from those sales, an 11.5% increase year over year.

Zoom out further and the scale gets harder to ignore. Statistics Canada estimates the broader cannabis sector — cultivation, processing and retail combined — contributed close to $11.6 billion to Canada's GDP in 2025. Licensed retail alone added just under $1 billion of that total, up 5% from the year before.

Despite those totals, Canada's cannabis retail sector isn't consolidated the way many investors might assume. Statistics Canada counted 3,295 cannabis retail businesses with employees at the end of 2025. Just over half, 51.4%, were small operations employing four people or fewer. Only two retailers nationwide employed between 200 and 499 people.

That fragmentation matters. With thousands of small, independently run dispensaries competing for the same customers, differentiating on price alone is getting harder to sustain. Increasingly, the edge is shifting toward whoever can get product to a customer's door fastest.

Consumer data backs this up. In Statistics Canada's most recent national consumption survey, 71.7% of cannabis users said they buy exclusively from legal sources. Product safety was the top reason cited, at 38%, but convenience ranked second at 16.9% — ahead of simply wanting to follow the law, at 12.9%.

That's notable because convenience is something a retailer can actively build, unlike trust, which takes years to earn. Household spending on legal, non-medical cannabis overtook illicit-market spending back in 2020, and the gap has only widened since — a trend that tracks closely with the expansion of same-day and scheduled delivery across major Canadian cities.

For Canada's many small retailers, delivery has stopped being a customer-experience add-on and become something closer to a structural requirement. A storefront in a saturated urban market carries fixed costs — rent, staffing, inventory shrink — that are hard to offset once margins compress. A delivery-first or delivery-supplemented model lets an operator compete on convenience without necessarily competing on storefront square footage.

That shift in priorities shows up in where industry investment is going. Instead of opening new physical locations, a growing share of retailers are spending on dispatch software, age-verification systems and route optimization built specifically for regulated products.

Some of that investment has come from outside Canada. Drop Delivery, a U.S.-founded delivery-management platform, expanded its white-label e-commerce and dispatch software into British Columbia, Alberta and Ontario back in 2020, betting that Canadian retailers would need the same infrastructure already in demand south of the border.

British Columbia, where the legal market has operated since 2018, shows this pattern clearly. Trade publication StratCann reported the province's private retail store count grew from 512 to 522 over the past year, even as the average price of cannabis kept sliding toward roughly $3.75 a gram. In a market where physical footprint isn't expanding quickly and prices keep compressing, a retailer's ability to extend its reach through delivery, without opening a new location, becomes one of the few growth levers left.

Vancouver-based cannabis dispensary is one example of how businesses are adapting to changing consumer expectations. By combining same day cannabis delivery Vancouver with a broader mail-order offering, the company reflects a wider industry trend toward convenience-first purchasing experiences.

The shift toward delivery is occurring alongside broader changes in consumer purchasing behavior. Much like food delivery and e-commerce transformed retail expectations, cannabis consumers increasingly expect products to be searchable, purchasable, and deliverable from their phones with minimal friction.

For retailers, this means the digital storefront is becoming just as important as the physical one. Online menus, live inventory visibility, streamlined checkout experiences, and reliable digital cannabis retail are increasingly influencing where consumers choose to shop. Operators that invest in user experience and fulfillment infrastructure may be better positioned to compete as convenience becomes a larger part of the purchasing decision.

Industry observers expect that wager to keep paying off for operators who treat delivery as core infrastructure rather than an afterthought. A year-end review of Canadian cannabis retail published by trade outlet StratCann pointed to consolidation among larger chains running alongside continued differentiation by smaller, more specialized retailers heading into 2026 — a dynamic in which logistics capability functions as both a retention tool and a competitive moat.

Regulatory developments will also continue shaping how the industry evolves. While Canada's framework differs from U.S. state-level systems, looking at regional updates like the evolving Nevada consumer cannabis regulations illustrates how local mature markets must constantly adapt as buyer expectations and compliance standards shift.

The federal numbers point to a market that is no longer defined by legalization alone. Canada's legal cannabis industry continues to expand, but growth is increasingly being shaped by how efficiently retailers can serve evolving consumer expectations.

As competition intensifies and margins tighten, convenience is emerging as one of the clearest differentiators. For many retailers, delivery is no longer simply a service feature — it is becoming a core part of how customers discover, purchase, and remain loyal to cannabis brands. The businesses that treat logistics, digital ordering, and fulfillment as essential infrastructure rather than optional add-ons may be best positioned for the next phase of industry growth.

Comments (0)